I reproduce here, a note to my very good friend, Jordan Lindsey of Conquer Trading, at YouTube, as a comment at his last video titled: Market View: Nasdaq & S&P 500 Technical Analysis, How Much Pullback Before You Buy?

‘Dear Sensei Jordan, I did some figures this morning, with both you and Michael Norman in mind (MMT, YouTube):

.

.

We ALL already know that valuations are at nosebleed levels. Yet its a matter of degree, not of kind. With no criticism to anyone here, for if we are to downgrade anyone, better it be me, not others or you. There just HAS to be more too it, than lines for support and resistance. Nevertheless:

.

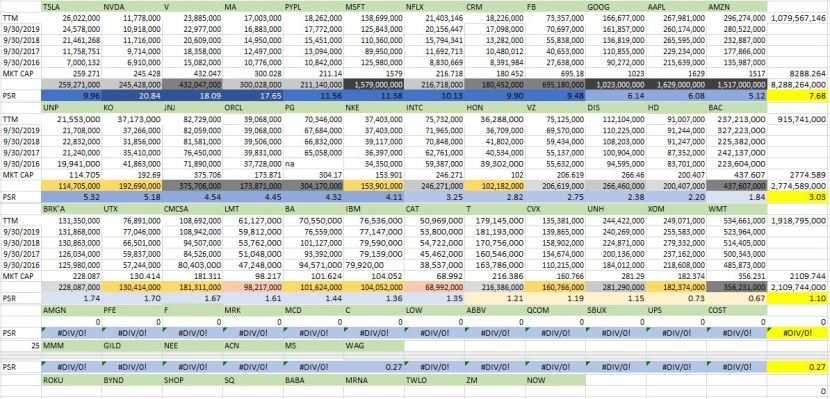

When you take any of the top ten ‘Go-go stocks’ such as TSLA, then of course the other biggie S&P companies such as AAPL, AMZN, MSFT, GOOG, FB, NVDA, NFLX, V, and PYPL, aggregate their market capitalization, comes to 7.75 trillion. Not for an economy. No. That would be too easy. A small set of dominators, in this oligopoly or plutocracy run by psychopaths (cf Chris Hedges, Dahr Jamail, Noam Chomsky, Stuart H. Scott, Paul Beckwith).

.

(yahoo finance. Just as we can say, Outlook is nearly the ONLY program MSFT ever sustained and managed not to completely ruin, with maybe Excel a close second, Yahoo managed to loose its excellence, yet their financial data reporting while not as good as what it used to be, is–like their sports data, still very good–quite good. cf ‘Income’ and Summary’).

.

Then aggregate the sales, which comes to 1.06 trillion, for a PSR of 7.7. Ten or twenty years ago, a price to sales ratio of 3.0 or 4.0 was considered VERY rich, say, for Peoplesoft or Siebel or Veritas, so on, among many good examples).

.

With the acceleration of change, and disintermediation of money, that has gone on–i.e. you deposit 1k to bank, they loan it out, then THAT money is loaned and the circle jerk just goes on, until nearly no one can remember, how it is that we got HERE. Not just inflation, but, so much money, which in turn, is turned into money, until nearly no one can quite remember, how it is, that we got here.

.

Yet if you take, the never mind, USA or EAFA or whatever poison you care to measure, lets say, THE planet is valued at 85 trillion (not now. Yes, I have it in Excel, not some stupid figure from USA Today or Huffington Post, etc), my own data. Call it 78, or 81, or 83 or 87, whatever, the comparisons remain and we place the super concentration into the NQ or Nasdaq 100 is placed into resolution:

.

The USA is about 40% of this, what I wryly like to call ‘the planet’. Gosh. Of that, about 80% is in the S&P 500, which means puts America at 34t, means SPX is 27 trillion (NYSE and Nasdaq. Used to be 8 or 9,000 public companies, now 6,450.

.

Here is where it gets interesting: in the S&P and has more or less been this way, since at least 1994, HALF the value of the S&P is occupied by no more than fifty companies, at times nearly forty. That puts us at $17,000,000,000,000 for THOSE forty or fifty companies. Of those, these ten are worth 7T.

.

Will not last. Its true I was up 330% for the last seven weeks, from starting capital. That is no longer true. Lets get real, keep it real. I am not perfect. After thirty years+, I am still not 100% in all ways. ‘Nothing is so expensive, as a real education’ (life education). And yet, I am not done yet. I see these numbers, and cannot believe, a PSR or 7 is permanent, no matter how breathless wonderful the Fed or Powell put is…

.

Lastly, not sure if it helps much, to add PG, HD, XOM, etc, but plan to compare these top 9 SPX companies–TSLA of course, duly NOT in the S&P, but will compare and report more, another day. Whatever it is, 7 x sales is an extreme abnormality. Means sales must double to get to 3.5 and as markets value goes up, and if it goes up, will not work in tandem, no more than GE, WSX, S, WCOM, AIG kept their mantle.

.

To be continued.

———- ———-

Knowledge manager, who can create, plan, furnish, operate, refine, and deliver complex processes involving people, products, results.

Leave a comment